By Antonio Hill

Somebody told you to diversify. A parent, a coworker, an advisor, something you read at 2am on Reddit. Spread it around, don’t put all your eggs in one basket. It sounded responsible, so you did it and never questioned it.

The part that they didn’t mention is that if you are under 25 with decades of compounding ahead, that one piece of advice is quietly costing you close to half a million dollars. Not because diversification is wrong. Diversification is one of the most important ideas in investing. But there is a massive gap between the kind that actually protects you and the kind that quietly bleeds your returns for 20 or 30 years. Most people are doing the second kind and feeling good about it.

Nobody showed them the bill. Let’s add it up.

What Diversification Actually Means (and the Kind That’s Quietly Robbing You)

Diversification means spreading your money across assets that don’t move together, so when one drops, the others don’t necessarily follow. That’s the concept. Simple enough.

What most people do in practice is something else. They grab the word and spray it across every asset class they can find. Stocks. Bonds. Cash. Real estate funds. International. Crypto. Maybe a little gold because somebody on a podcast mentioned it.

That’s where the damage is. There are two completely different types of diversification and people blend them into one fuzzy idea of “being safe.”

The two types most people confuse

The first type is diversification within stocks. Owning hundreds or thousands of companies instead of one or five. Amazon tanks but Microsoft soars and you barely feel it. This is the good kind. It works exactly as advertised, and you should do it (in my opinion, of course).

The second type is diversification across asset classes. Spreading money into bonds, cash, real estate, the whole buffet. For someone in their 30s building toward early retirement, this is where the money quietly leaks out.

Bonds don’t move with stocks. True. But the reason they don’t move together is that they also don’t grow together. Adding bonds lowers your volatility. And somewhere along the way you got sold the idea that lower volatility means lower risk. It doesn’t. Those are two different things, and confusing them is the most expensive mistake on this page.

Volatility is not risk

Volatility is noise. Here’s a clarification, too: what matters isn’t how long until you retire. It’s how long until you actually spend the money. Those are two different clocks. If you’re aiming to retire early your accumulation runway is short, sure. But the dollars you invest today don’t get spent for decades, and some of them not for 40 or 50 years, because an early retirement has to last that long. So a market crash on money you won’t touch until your 70s isn’t a threat. It’s a sale. Every dollar you put in during a crash buys more shares at a lower price, and those shares ride back up with the market. Treating a temporary price drop like an emergency, and buying bonds to protect against it, means you’re defending against a problem you do not have yet.

If the money has long enough to sit before you spend it, volatility literally cannot hurt you unless you panic and sell. So the real question isn’t how to kill volatility. It’s how not to panic when it shows up. Different problem. Different solution.

I learned that one the hard way, and I’ll get to it.

The Real Cost, With Real Numbers

Opinions without numbers are just noise. So let’s put actual money on the table.

The S&P 500 has averaged roughly 11% a year over the last 40 years. The Nasdaq 100 has done about 15% a year over that same 40 year stretch, and closer to 18% over the last 10 years, carried by tech. A 60/40 stock and bond mix has averaged about 8%.

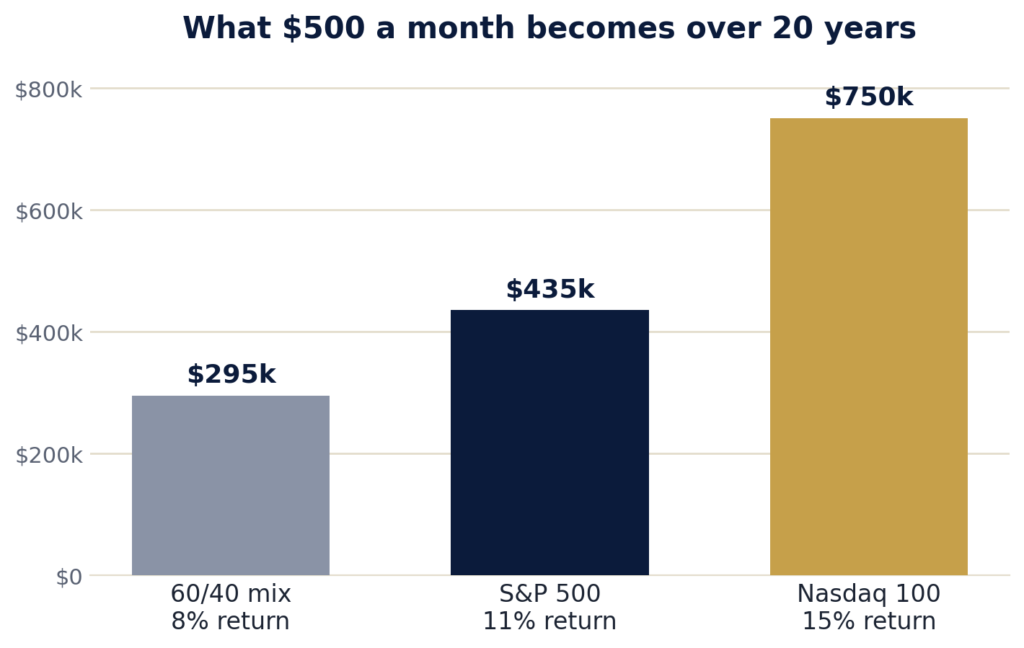

Now take $500 a month, invested every month for 20 years, and run three versions of the same person.

At 8%, that $500 a month grows to roughly $295,000. At 11%, it’s about $435,000. At 15%, it’s about $750,000.

Look at that gap. Same paychecks, same discipline, same 20 years. The only difference is how much “safety” they bolted on. The 60/40 investor didn’t dodge some catastrophe. They dodged paper volatility on the way to retirement and paid for the smooth ride with a chunk of their future.

What you actually traded away

The person who earned 8% instead of 11% gave up about $140,000 compared to someone who just held the S&P 500. Compare them to the heavy Nasdaq investor and the gap is close to $450,000. On $500 a month. Same contributions, same timeline, wildly different life.

That 60/40 portfolio your advisor called “responsible” has historically returned around 8% a year. The S&P 500 alone, around 11% over those same 40 years. That difference compounds into a number that changes when you get to stop working. And the person who held the 60/40 didn’t lower their risk in any way that matters over time. They lowered their wealth, and the scary part is that they felt good about it.

Rethinking your allocation right now? Good. The free guide, 10 Quiet Mistakes That Kill Your Early Retirement, walks through the quiet ones exactly like this, the errors that don’t feel like mistakes while you’re making them and cost you years.

Who Bonds Actually Protect

Let me be clear before I get accused of saying bonds are trash. They aren’t. Bonds do a real job for specific people in specific situations. This isn’t “bonds are useless.” It’s “bonds are being sold to the wrong people.”

If you’re within 5 to 10 years of your retirement date and a major crash would genuinely blow up your timeline, bonds make sense. They reduce volatility, and if a 40% drop in year one would create a catastrophic sequence of returns problem, holding some is a rational call. That’s the scenario they were built for.

There’s also the person who, emotionally, cannot stop themselves from selling when the market drops 30%. For that person, bonds aren’t really an investment. They’re a behavioral seatbelt that keeps them from driving the portfolio into a wall. If that’s you, be honest about it. Just know exactly what the seatbelt costs.

Here’s the thing about who the standard advice was built for. Advisors baked bond allocation into the default because they were advising a much broader audience. Shorter horizons. Lower risk tolerance. People who really would panic and sell at the bottom. That advice is calibrated for the average investor.

I have a feeling that’s not you.

You’re reading a site about retiring early. You earn well. You already think about money differently than almost everyone around you. Running the average person’s playbook is like following a workout built for a sedentary 65-year-old and wondering why you’re not getting any faster. It was never written for you.

Why Your Time Horizon Changes Everything

Every 20 year rolling period in S&P 500 history has produced a positive nominal return. Every one. Crestmont Research, which tracks market data going back more than a century, has documented it. JP Morgan’s Guide to the Markets shows the same pattern. Not one 20 year window in the recorded history of the index ended negative.

Sit with what that means for you.

If you invest a dollar today and leave it alone for 20 or 30 years, history says it makes money. Not probably. Not if the stars align. Every 20 year window came out positive. And notice that has nothing to do with when you retire. It’s about when you spend that particular dollar. The money you’ll live on in your 60s and 70s gets its full 20-plus years no matter how early you walk away from work.

The 2000 tech crash was the worst stretch for the Nasdaq in modern history. The recovery from the March 2000 peak back to a new high took about 15 years, into 2015. Sounds brutal, and it was, if you were retiring in 2000. For someone with a 30 year horizon who kept buying? That 15 years was a rounding error. You bought shares cheap the whole way down and the whole way back up, and you came out ahead of every investor who fled to bonds and waited for the green light.

Those investors missed the recovery. And a lot of them missed it while paying someone 1% a year to watch it happen.

Here’s another number worth sitting with. Miss just the 10 best trading days over a 20 year stretch and your return gets cut roughly in half. The best days almost always land right after the worst ones, so if you bailed to cash during a crash, you didn’t just miss the bottom. You missed the snapback that follows it. JP Morgan ran the numbers and the result is ugly for market timers.

The real question isn’t what happens if the market drops. It’s what happens if you’re not fully invested when it rips back up.

And the sequence of returns risk people keep citing as the reason to hold bonds? Real, and if you’re retiring early it shows up sooner for you, since you stop contributing sooner. But it only bites once you start withdrawing, not while you’re still piling money in. Loading your whole portfolio with bonds at 33 to defend against a risk that lands at 40 means dragging your returns for years and arriving with a smaller number, right in the window where growth mattered most. There’s a sharper tool for that, and it’s coming up.

You’ve got decades of compounding in front of you. Act like it.

The Financial Advice Industrial Complex

Let’s be real about something that doesn’t get said enough.

The diversification advice most people got wasn’t built to maximize their wealth. It was built to protect the person handing it out.

Advisors typically charge around 1% of assets under management every year. On a $500,000 portfolio that’s $5,000 a year, plus the compounding loss on that $5,000 every year after. Over 20 or 30 years, that fee drag quietly destroys a staggering pile of money that should be yours. I grew up watching my parents live paycheck to paycheck, so paying someone five grand a year to underperform a free index fund is the kind of waste that makes my eye twitch.

Here’s the data. About 92% of active funds underperformed the S&P 500 over the last 20 years, according to the SPIVA Scorecard from S&P Global, which has tracked this every year for two decades. The overwhelming majority of professional stock pickers, people whose entire job is to beat the market, do not beat the market over any meaningful stretch. Betting your retirement on the rare manager who does is like betting it on a bench player outscoring prime LeBron on a random Tuesday. Could happen. You wouldn’t bet 1% of your future wealth on it, though.

So you’re paying 1% a year to someone whose fund will probably lose to an index fund you could hold for 0.03%. And in exchange for that 1%, they tuck you into a conservative bond allocation that drags your returns down further. You lose on the fee. You lose on the allocation. And it gets called financial planning.

Warren Buffett understood this and said so out loud. In his 2013 letter to Berkshire Hathaway shareholders, he laid out what he wanted done with the money left in trust for his wife. The instruction was simple. Put 90% in a low cost S&P 500 index fund and 10% in short term government bonds. In his words, the trust’s long-term results “will be superior to those attained by most investors” who pay high-fee managers. Read it yourself in the 2013 Berkshire Hathaway shareholder letter.

The greatest investor alive told his own estate to go 90% into an S&P 500 index fund. Not a hand-picked basket. Not a guy charging 1%. An index fund. For a trust meant to support someone who might already be retired.

The reason conservative advice is everywhere isn’t that it’s right for you. A 100% stock portfolio that drops 30% in a year is a brutal conversation for an advisor to have with a nervous client. A balanced portfolio that drops 15% is an easy one. The advice got built around that conversation, not around your account balance after 20 years of compounding. You’re paying for their comfort.

What Smart Diversification Actually Looks Like

So what do you actually do?

Diversify within equities. Own hundreds of companies, not one or ten. A total market index fund does this automatically for almost nothing. A Nasdaq weighted fund gives you the same breadth with a heavier dose of the sector that’s driven the economy for two decades. Both beat the large majority of active managers over any real horizon. Neither asks you to pick a winning stock or hand anyone 1%.

If you want a starting structure, the three fund approach is hard to beat for most people. A US total market index fund as your core. An international index fund for global exposure. A small bond slice only if you’re genuinely within 10 years of your target date. That’s the whole plan. No advisor, no fancy rebalancing, no hidden fees nibbling your compounding. You set up the auto-transfer from your paycheck to your brokerage (assuming that’s your early retirement bridge account), and GGs.

My own approach during accumulation is 100% equities. Heavy Nasdaq and total market. No bonds until I’m actually close to walking away from full time work. The time horizon data backs this, and honestly I’d rather ride out the volatility than show up to retirement with $500,000 less than I could have had.

Now, the honest tradeoff, because I’m not going to pretend my tilt is free. A heavy Nasdaq tilt isn’t really diversification. It’s a concentrated bet that big tech keeps leading. That bet has paid for the last 15 years. It also went the other way for the 15 before that, when the Nasdaq fell almost 80% in 2000 and took until 2015 to climb back. So if you tilt heavy, know what you’re doing. The reason I’m fine with it during accumulation isn’t that tech can’t have another lost decade. It’s that I’ve got two things that cancel one out. A time horizon I can manipulate, and the proven discipline to keep buying through a crash instead of selling into it. Take either of those away, and a broad total market index is the smarter call. No shame in it. It’s still going to beat your neighbor’s advisor.

When retirement actually arrives, the bucket strategy does the job bonds were supposed to do without strangling your growth engine. Keep about three years of expenses in cash or cash equivalents, sized against the account you actually spend from, and leave the rest fully invested. That cash covers the bad years so you’re never forced to sell stocks at the bottom. The rest keeps compounding. You get the sequence of returns protection without the decades-long return penalty. Buffett’s own 10% short-term bond slice is the same idea, by the way. It’s there so his wife isn’t selling stocks at the wrong time.

If you’re retiring early, here’s the one adjustment that matters; as you close in on your date, build a buffer. About three years of expenses in cash and short-term bonds, parked in the last couple years before you quit and held into the start of retirement. That’s not a decades-long bond drag. It’s targeted insurance for the only stretch where sequence risk can derail the whole plan, the first few years of withdrawals. Pair it with a retirement date you’re willing to nudge by a year if the market craters right before you pull the trigger, and you’ve covered the real risk of a short runway without capping your growth the whole way up.

In my opinion, here’s what someone in their 20s or 30s needs to hear. If you’re disciplined, you won’t panic sell in a crash, and the bulk of your money is decades from being spent, which it is even if you retire at 40, you do not need a bond-heavy portfolio right now. You need a growth engine now and a cash buffer later. That’s not reckless. It’s the position the data supports for someone at your stage.

So let’s go back to the actual question. Everyone should diversify. Spread across hundreds of companies, across sectors, across the US and international markets. That kind works and it matters.

But the question was never whether to diversify. It’s whether you should diversify away from growth at the one moment in your life when growth is the only thing that matters. You get one window where compounding runs at full speed. The years when you’ve got decades ahead and volatility is just background noise. Bolting bonds onto that window doesn’t make you safer. It makes you poorer.

I found out something similar personally. In March 2020 I opened my brokerage, put in $10,000 as COVID was tanking the market, and then got scared and let it sit in cash for two months while the market ripped back up without me. I missed most of the rebound. That one mistake taught me more about the opportunity cost of not being invested than anything I’ve read since, and I’ve watched for it ever since.

If you’re rethinking your approach, the full story of how I built toward seven figures in my 30s goes into exactly what I did and what I got wrong, that COVID mistake included.

Frequently Asked Questions

Do I need bonds in my 30s?

If most of your money is decades from being spent, you’re disciplined, and you won’t panic sell in a crash, no, and that holds even if you’re retiring early. An early retirement still has to fund 40 or 50 years, so the bulk of the money keeps a long horizon. Bonds lower volatility, but volatility is not the same as risk when you have decades to recover. They start earning their place as you get within 5 to 10 years of your target date, in the form of a cash and short-term bond buffer, or if you honestly know you’ll sell in a downturn. Until then they mostly just lower your long-run returns.

Is a 60/40 portfolio too conservative if I’m retiring early?

During accumulation, yes, for most early-retirement savers. A 60/40 has historically returned around 8% a year versus about 11% for the S&P 500. On $500 a month over 20 years that’s roughly $295,000 versus $435,000. The 40% in bonds buys a smoother ride you don’t need yet and costs you a large chunk of your nest egg. Closer to retirement, a bond or cash buffer makes much more sense.

Is 100% stocks too risky?

For a young accumulator with a long horizon, the bigger risk is usually being too conservative. Every 20 year rolling period in S&P 500 history has ended positive in nominal terms. The real catch is behavioral. 100% stocks only works if you actually keep buying through a 30% or 40% drop instead of selling. If you know you’ll panic, that’s exactly when a bond allocation or a cash buffer makes sense.

Nasdaq 100 or S&P 500 for the long term?

Both are broad, low-cost, and beat most active managers. The Nasdaq 100 has returned more over the last 40 years, around 15% versus 11%, but it’s concentrated in tech, so it’s a more volatile bet on that sector continuing to lead. It fell almost 80% in 2000 and took 15 years to recover. A total market or S&P 500 fund is the more diversified core. A Nasdaq tilt is a deliberate bet, fine if you understand the tradeoff.

One offer, same as up top. If you want the free guide, 10 Quiet Mistakes That Kill Your Early Retirement, and a clear look at where you actually stand, grab it here. About 10 minutes, and it will probably move your timeline up. Send me the guide.

This is a voice piece, my own opinion and analysis, not personalized financial advice. The free guide above puts you on my email list, where I also sell The Early Retirement Blueprint. I am not compensated by any fund company or advisor mentioned here.