By Antonio Hill

My friends used to get so annoyed at me in college. We’d be thinking about going out, somebody would suggest doing just about anything, and before they could even finish the sentence, I was already saying it. “Uh, that costs money.” Gas? Costs money. Going to the movies? Costs money. Literally just existing near a place that charges for things? Costs money. We can just chill here. “You won’t meet any girls here, though.” Ok, that actually worked sometimes.

I was not frugal. I was cheap. I always had been, and I knew it.

Fast forward to right now. Thirty-three years old. Just under a million dollars in investable assets. No inheritance. No lucky crypto run. No company I started. I did not go viral. I just had a system, and I stuck to it even when it was painful, even when it was genuinely hard, and even when I wanted to quit. That system worked. And now I have more conviction in it than ever, because I have watched it work with my own money for a decade.

If you are a high-income earner in your 20s or 30s who is already tired of the corporate grind and wants to retire early (way before 65), this is exactly how I built real wealth by my 30s.

Where I Actually Started

I grew up in Mississippi, and I have lived in four states since. My parents were good people and I love them, but financially they were pretty much exactly like most American families. Paycheck to paycheck. Sometimes a little more than that. Get a bonus, buy something nice or take a good vacation. Nothing wrong with it. But there was no real financial education at home, and talking about money was just not something families like mine did. It was not a priority. You had dinner together, you had family time, and money was just sort of this invisible thing in the background that nobody talked about directly.

I can tell you the exact shape of it though. I came home from basketball practice one afternoon and my mom was screaming at me over nothing. I was an annoying kid, so getting yelled at was not new, but this was different and I could not work out what I had done. Turns out it was not me at all. She had a bad day at work, she and my dad were in a rough stretch that week, and a bill had shown up that the paycheck could not absorb. Three things landing at once.

Here is what I took from it years later. You do not control how your workday goes. You control even less about another whole person. But you have almost total control over how prepared you are with money, and that is one entire category of stress you can just delete from your life. I did not decide anything that day. I just filed it.

I got a full scholarship to college. So, I had zero reason to take on any debt. I took out about eight or nine thousand dollars in student loans anyway because I wanted to live off campus for a semester. I still have not paid that loan off. And before you say anything, there is a reason for that. The interest rate on it is four percent. The market has averaged over 10% historically in broad indexes, and considerably more in the Nasdaq over the last decade. I am not paying off a four percent loan with cash I could have working harder for me. The math does not support it. Same reason I am not paying off my mortgage early.

I graduated in 2016 with a mechanical engineering degree and started my first job two weeks later making about $90,000. I was single, I was in a low cost of living area, and as mentioned before, I was cheap. I had a lot of disposable income for someone my age. But here is the thing. I had zero idea what to actually do with it. I knew I didn’t want to waste it. I knew I wanted my money to work harder than it was sitting in a savings account. I just did not know yet what that actually meant or how to do it efficiently, and I was honestly scared of messing up.

That gap between knowing you should do something and actually knowing how to do it right cost me more than almost any other mistake I ever made. More on that in a minute.

What Building Wealth in Your 30s Actually Looks Like for Most People

Before I get into the how, I want to put the result in context so you understand what we are actually talking about here.

The Federal Reserve’s 2022 Survey of Consumer Finances found that the median retirement savings for Americans between the ages of 35 and 44 is roughly $45,000. The entire balance…after years of working. For people who are already approaching their 40s.

That’s the median. Half of Americans in that bracket have less than $45,000 saved for retirement. Now I want you to think about what $45,000 actually buys you in retirement if you follow the standard 4% withdrawal rule. That is $1,800 per year. A hundred and fifty dollars a month. That’s it.

This is not me trying to scare you. This is me showing you what the default path actually looks like for most people, because most people have no idea. And if you are a high income earner reading this right now, the gap between where you could be and where the average person ends up is not just about what you make. It is about what you decide to do with it. The short version is that working until 65 is a default, not a plan, and defaults are for people who never questioned whether there was a better option.

Why I Changed My Game in May 2020

I had always been “fiscally responsible” (cheap), but being cheap and having real intent with money are two different things.

Around May of 2020 is when I forced myself to start. I had moved $10,000 from my savings into a new brokerage account on March 17th, right in the middle of the COVID crash, but I did not invest a single dollar of it for two months because I was scared. The research was obvious. All of my research told me the selloff was overdone and the market was on sale. But knowing something intellectually and having the conviction to act on it are two completely different things, and I did not have that conviction yet. The money just sat there while the market started recovering without me.

The gains I left on the table by waiting those two months are painful to think about to this day, but it was the first powerful lesson of many I would learn on this journey. I had been working for a few years at that point, saving decently, but not with any real direction or intention behind it. And I started doing the math on what my actual life could look like if I got serious. Not just saving money, but building real wealth fast enough to walk away from corporate America on my own terms before I was old.

I’ll let you in on the truth about the professional world that nobody told me at 23. Working hard is not the main thing that gets you ahead inside most organizations. What gets you ahead is who you know, how well you play the politics, and how skilled you are at managing perceptions up the chain. I did not understand that at first. And then when I did understand it, I wanted even less part in it. You’re telling me not only do I have to do this full-time job, but I have to play politics while I’m doing it? I’m an introvert. That’s not a skill I was interested in developing. The idea that I was going to spend the next 40 years navigating that, waiting for raises that were never quite enough, watching promotions go to whoever was best at the game, genuinely turned me off.

So I asked a different question. Not “how do I move up faster inside this system.” Instead I asked “how do I make this system unnecessary?”

JL Collins, who wrote The Simple Path to Wealth, put the whole point of it into one line. “There are many things money can buy, but the most valuable of all is freedom. Freedom to do what you want and to work for whom you respect.” That idea hit me so hard the first time I came across it. Not because it was complicated. Because it was obvious, and I had never heard anyone around me actually living by it.

I also did a simple life expectancy exercise around this time. My family history puts me somewhere in my mid 80s realistically. If I work until 65, I get maybe 20 years of freedom after that. And not all of those years are going to be good years. Not all of them will be years I can travel, spend time with family, stay up late doing exactly what I want. Some of those years I’ll be too tired, too sick, or both. Twenty years is what you get for handing over the best four decades of your life. That math does not work for me.

My plan is to retire at 40. I will break down the math in another article, but everything comes back to three variables.

The Three Levers

I talk about this constantly because it is the foundation of everything. Building wealth in your 30s fast enough to retire early comes down to three things and three things only. Time in the market, how much you contribute, and your return rate on investments.

That is it. Pull all three hard and retire extremely early. Pull them half-heartedly or wait to start and you work until 65 like everyone else. The math is not complicated and it does not negotiate.

The part that sucks – if I had started doing what I do now from the very first day I got my first paycheck at 23, I would be retired right now. I have done the math on this more times than I can count. I would be done. The six years I spent being financially inefficient, saving but not with real direction or a real system, that was a third of my planned working career wasted on being disorganized. Time is the one lever you cannot get back.

Lever One. Start Before You Feel Ready.

I opened my first real investment account at 23. It was my 401k. At 23, I barely knew what a 401k was, and I didn’t really figure it out until a bit later. But someone showed me a compound growth chart and it scared me into action immediately.

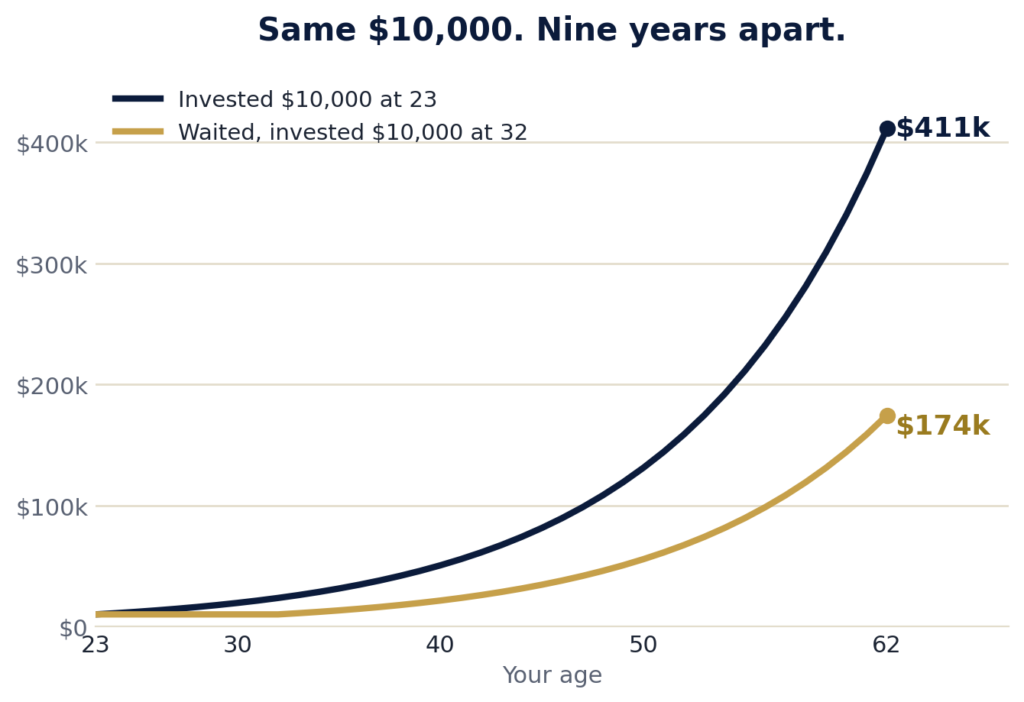

Here is a concrete example of what that early start is actually worth. If you invest $10,000 at age 23 and earn an average 10% annual return, that single contribution compounds to roughly $410,000 by age 62. Wait until 32 to make that same $10,000 contribution and you’re looking at about $174,000. Same money. Same market. Nine years earlier. More than double the result.

I was not efficient with my investing right away. I know that. But having money in the market at all from a young age still mattered enormously compared to sitting on the sideline. Every month you wait is a month that money is not compounding for you. Compound interest does not care how motivated you feel. It just runs.

Lever Two. Contribute More Than Feels Comfortable.

I target contributing 40% or more of my income every year. Right now my wife and I bring in about $200,000 combined. She works as well and she is fully on board, which I will come back to because it matters more than most finance communities admit. Together we contribute aggressively toward a shared goal.

The trick that made the contribution rate automatic instead of painful was setting up transfers the day after each paycheck. Before I could see the money. Before I could decide I needed something. It was just gone into accounts working for us.

According to Vanguard’s How America Saves data, only 14% of people with a 401k actually contribute the maximum each year. The IRS 401k contribution limit for 2026 is $24,500. Eighty six percent of people leave tax advantaged, legally protected, compound growth on the table every single year. I maxed mine from about age 24 until about age 30. At this point, I had reached coast FIRE, meaning I had invested enough early that compounding alone would carry me to a normal retirement even if I never added another dollar. There is a second test that runs the other direction, how much pretax money is too much, and it decides when you should stop feeding that account. To this day, I put money in to get my employer’s match. Even though I don’t need it, free money is free money.

And the 401k is just the beginning. Max your HSA if you have a high deductible health plan. That thing is a triple tax advantage account most people sleep on. I do not have one in my current job, and I hate that I can’t contribute to my existing one anymore. Contribute to your Roth IRA. After those are maxed, everything left goes into a taxable brokerage account. There is a specific order to this, and I have a system for how I think about it. Every dollar needs a job. If that job is not feeding your family, housing your family, or building your future, it is leaking out and doing nothing.

Lever Three. Your Return Rate Is a Choice You Make.

The default advice has always been to diversify broadly, add bonds, play it safe. And if you are already 62 and drawing down your portfolio, some of that actually makes sense. But if you are 28 years old with 12 years until your target retirement date, putting money into bonds earning 3.5% while inflation runs near that same number is like pressing the brakes in a race and calling it a strategy. You are slowing yourself down on purpose.

I am 100% in equities. No bonds. Full disclosure, I also hold some individual stocks in companies I have done serious research on, and I mean thousands of hours of it, not a Reddit thread and a feeling. But read this part carefully, because it is not me telling you to go pick stocks. It is the opposite. Stock picking is a different game, it takes a different temperament and an absurd amount of work, and for you, like for almost everyone, the right move is a low cost index fund and nothing fancier. I keep the individual stuff in the background here on purpose. The Nasdaq 100 has averaged roughly 13% annual returns over the last 20 years and closer to 18% over the last 10. With AI and technology growing the way they are, I think those numbers hold or climb over the next decade. Just my opinion.

Yes, the market drops. Sometimes significantly. But the truth is there is not a single 20 year rolling window in the entire recorded history of the US stock market where a broad index investor who left their money alone lost money before inflation. Not one. All a market dip is is everything you planned to buy going on sale. The smart move is to buy more, not sell.

What people call risk, I just do not see as risk. If you genuinely believe the US market could go to zero and never recover, fine. But then you shouldn’t be investing in anything at all, and you’re probably not the audience for this. If you believe what the last 100 years of market history shows, which is that it has always come back so far, then what exactly are you protecting yourself from by going conservative at 30?

Want the exact list of silent killers for your early retirement dreams that I wish I had earlier? I put together a free guide for 10 Quiet Mistakes That Kill Your Early Retirement that walks through all of them. This is the resource I wish someone had handed me when I was 23 trying to figure out what mistakes I was even making.

What I Actually Invest In and the Student Loan Thing

Low cost index funds. That is the whole answer for you, and honestly it is most of the answer for me too. I do hold a slice of individual equities in a few companies I have extremely high conviction in, but treat that like a footnote, not the playbook. The index funds are the playbook.

And I know that sounds too simple. People always want the complicated answer because complicated feels like it means you’re being more serious or more careful. But complexity in investing almost always costs you money. More trades means more realized taxes, and more chances to make emotional decisions. Emotional decisions are the number one reason most people and most institutions don’t beat the market over time.

S&P Global’s SPIVA Scorecard found that over a 20 year period, more than 92% of actively managed US equity funds underperformed the S&P 500 after fees. Not a small group. Over nine out of ten professional fund managers, people who do this full time, underperform what you could do yourself by putting money in an index and leaving it alone. The financial advisor thing deserves its own section, but that stat is the whole argument.

And the student loan I mentioned earlier. Four percent interest rate. I can have that cash in the market instead earning double that at a minimum. I pay the minimum on the loan and invest the rest. I will pay it off whenever I feel like it, which might be never. Same philosophy applies to my mortgage. Paying off a low interest loan early when the market is offering around 10% average annual returns is just bad math.

What I Cut Out and What I Kept

There is a whole section of the FIRE community that tells you to gut your entire lifestyle now, eat peanut butter sandwiches and ramen, never spend a dollar on anything enjoyable, and then after decades of that, retire at 35 to keep eating peanut butter sandwiches and ramen. That approach is crazy to me. You sacrificed so that you could…sacrifice more? Then you called it freedom.

The goal is to maximize your life. All of it. Not just the part after you stop working.

Here is how I actually think about spending. Every purchase gets one question. Is this genuinely adding meaning or substance to our lives, or is it just easy to spend? If it’s real value, spend it without guilt. A family vacation that my daughter will remember. A home in a good neighborhood with good schools. Food that is actually good. Things and experiences that actually matter to our family. Those get funded.

What got cut was the spending that created the appearance of a good life without actually building one. The brand new 2017 Corvette that I financed because it felt like what you do when you start making real money. Eating out for lunch with coworkers constantly because I wanted to get away from the office. Subscriptions quietly renewing every month totaling hundreds of dollars for things I barely used. Random stuff that accumulated in the house and added nothing to my life.

I plan for my retirement spending to be about 30% higher than what we spend now. That surprises people, and it is worth knowing that every step up in target lifestyle has a price measured in years, not dollars. But think about it. When you are retired and every day is a Saturday, you spend more money. You travel more. You do more. What people also don’t realize is that we don’t need our full working income to have the same lifestyle in retirement. We obviously won’t be contributing to our retirement portfolio anymore, which is a big chunk of where our money goes. Also, taxes will be a lot lower in retirement if you do it right.

Living below your means does not mean living small. It means being intentional about where the money actually goes.

The Marriage Factor and the Financial Advisor Question

The Marriage Factor

This one is uncomfortable to say but I would be doing you a disservice if I left it out.

The person you marry is probably the single most important financial decision you will ever make. It can accelerate everything or it can destroy everything, and once you’re in it, it is not an easy thing to change.

My wife works. She is fully on board with retiring early and what that means for our life, even if early retirement is more my obsession than hers. She understands why it matters. She supports the plan, and I truly appreciate her for it. Without that complete buy-in, the numbers look completely different, and not in a good way.

I got lucky in that I found someone who gets it. But luck is not a strategy. If you are not yet married and early retirement is your goal, treat financial compatibility as a serious filter, not an afterthought. A partner who does not share early retirement as a goal will systematically undo every lever you pull. That is not a small thing. It is a potential retirement date killer. Compromise is key.

The Financial Advisor Question

Do I use one? No. And I will not during the accumulation phase.

A standard financial advisor charges 1% of assets under management. With just under a million dollars invested, that is close to $10,000 per year going to someone else. Every year. But the real cost is not the fee itself. The real cost is the opportunity cost of what that $10,000 grows to if it stays invested over the next 15 years at around 10% average annual returns. Run that math and the number is genuinely painful.

And what do you actually get for it? The SPIVA data above already answered that. Over 90% of actively managed funds underperform a simple index over 20 years. Just because your parents used them for 20 years doesn’t mean that they are the exception. They do not have a magic formula. They manage your money conservatively, charge you a percentage of everything, and trail the market while doing it.

There are two legitimate uses for a financial advisor. One is behavioral coaching, which is basically someone talking you out of panic selling at the bottom. If you genuinely cannot stop yourself from doing that, fine, maybe that fee is worth it. The other is tax and withdrawal planning when you are getting close to pulling the trigger on retirement. At that point I would pay a one time flat fee to a fee-only financial planner to build a withdrawal strategy. One session. One fee. Not a percentage of my wealth every year forever.

Where I Am at 33 and What Comes Next

Just under a million dollars in investable assets. On track for 40. And the math at this point is where it starts getting cool.

At a 15% average annual return, which is what I have personally averaged over the last 10 years, my current balance roughly doubles every five years without contributing another dollar. But do not plan on 15%. That is my number, and it is juiced by the individual positions and the heavy tech tilt I just told you not to copy. Plan on something closer to 10% for a broad index and treat anything above that as a bonus. I will obviously keep contributing aggressively. Run the full projection out to 40 and the number my family can live off indefinitely, with a conservative withdrawal rate and a margin of safety built in, is well within reach. Run your own version in the early retirement calculator if you want to see where your date actually lands.

But here is what this is actually about. It is not the number. The number is just a proxy for options. Waking up and deciding what to do with my time. Being fully present with my daughter without the background noise of a job I have to get back to. My daughter is two years old right now. By the time she is nine, her dad is retired and present. That is the plan. That is the whole point of all of this.

And I want to be honest with you before I close. This path does not work for most people, and that is not me being dismissive. It is just reality. The Federal Reserve data, the savings rate data, every retirement readiness survey I have ever read, all of it points to the same conclusion. Most Americans will work until their mid 60s and hope Social Security is enough. That is the default. Most people are not wired to operate the way I’m describing here, and the earlier you want to retire, the harder the discipline gets.

But you are not here by accident.

If you are a high income earner who is serious about building wealth in your 30s, already thinks about money differently than the people around you, and genuinely cannot picture spending another 30 or 40 years inside corporate America waiting for 65, this is your path. The levers are real. The math works. The only variable is whether you actually execute.

Start now. Start today. The six years I lost by not committing and being inefficient were a third of my entire working career, and that cost me years. You do not want to find out what yours cost you.

If this landed, grab the free guide for 10 Quiet Mistakes That Kill Your Early Retirement. Three things control when you retire. How long your money has been in the market, how much you put in, and what rate it grows at. Every mistake in this guide attacks at least one of those. Some hit all three at once. Takes about 10 minutes to read. Probably the most useful 10 minutes you spend this week. Get the Free Guide.

Frequently Asked Questions

How much should you have saved for retirement by 35?

There’s no universal number, but here’s the context. The median American aged 35 to 44 has about $45,000 saved, per the Federal Reserve. If you’re a high earner aiming to retire early, you want to be a multiple of that. The honest answer depends on your target retirement age and your spending, not a generic benchmark. What matters far more than hitting a specific balance by 35 is your savings rate and how early you started, because those are the two levers you actually control.

Should I invest or pay off low-interest debt first?

If the rate is low, think a 3 to 4% mortgage or student loan, invest the surplus instead of rushing to pay it down. The long-run market return has historically run around 10%, well above a 4% loan, so every dollar you throw at that loan early is a dollar not compounding at a higher rate. The exception is high-interest debt like credit cards. Pay that off immediately, every time. It’s a math problem, not a discipline test.

Can you really retire early on a normal salary?

Early retirement is more about your savings rate than your income, but moving fast does take an above-average income. Someone earning $120,000 with a 40% savings rate and an early start is in a strong position. It isn’t about being ultra-wealthy. It’s about the gap between what you earn and what you spend, and what you do with that gap. The smaller the income, the harder the math, but the levers are identical for everyone.