Your FI number can be perfect. You can run the math ten different ways, hit the target to the dollar, and hand in your notice right on schedule. If the market drops 30% in the third month of your retirement, that perfect number won’t mean a whole lot.

That’s sequence of returns risk. In my opnion, it’s the single biggest threat to an early retirement. I also think it’s not that big of a deal if you have a plan. Both of those things are true at the same time, and this article is the math behind both. By the end you’ll have a loose version (still developing, obviously) of what I plan on doing, with the exact numbers, and you’ll see why the people yelling loudest about this risk are usually selling something.

What Sequence of Returns Risk Actually Is

Here’s the version I’d give you over a beer.

In retirement, your portfolio is your paycheck. The bills don’t pause because the market fell, so you sell shares to eat. And when you sell shares in a down market, that loss stops being a paper loss. It’s locked in. Permanent. Those shares are gone, they don’t get to ride the recovery, and every dollar you pull out near the bottom caps what your portfolio can ever become.

Sequence of returns risk is the risk that bad returns early in retirement, paired with the withdrawals you’re forced to take, permanently shrink what your portfolio can recover to. The order of your returns matters more than the average of them.

You already know the accumulation phase version of this rule. Never sell the dip. Buy it if you can, ignore it if you can’t, but never sell it. Sequence risk is what happens when retirement takes that choice away. You’re not selling because you panicked. You’re selling because it’s Tuesday and Tuesdays cost money.

When I first understood it, my reaction was that this is compounding’s evil twin. Compounding takes time and multiplies money. A bad sequence takes the same average return and quietly caps it, because the withdrawals did their damage while the balance was low. Same engine. Running in reverse.

The heavy pack problem

Picture climbing a mountain in blizzard country. You know storms are coming. You don’t know when. If a blizzard hits on day two, your pack is at its heaviest and you burn through supplies fast just to survive it, which leaves you thin for the entire rest of the climb. If the same blizzard hits near the summit, you’ve already covered the distance. Lighter pack, less to protect, less to lose.

Same mountain. Same storm. The timing decides whether it’s a story you tell or the reason you turned back. Your first decade of retirement is the bottom of that mountain.

And this is why I laugh a little when people polish their FI number to the third decimal. I care about the number, I wrote a whole piece on how much you actually need to retire at 40. But the number is a goal and a guardrail, nothing more. Your FI number can be as accurate as humanly possible, and if the market hands you a 30% drop in month three, the number won’t help you. The plan will.

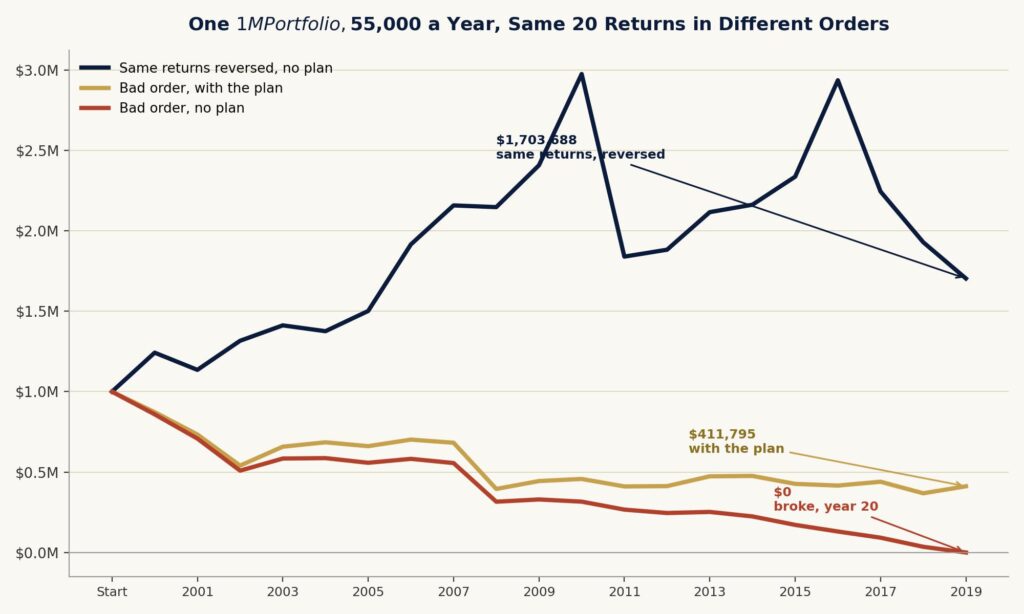

Same Twenty Returns, One Retiree Goes Broke

Let me show you instead of telling you.

I took the S&P 500’s actual annual returns from 2000 through 2019, dividends included, straight from the historical record. Twenty real years. They average 7.68% a year, which sounds like a retirement dream. Then I handed those exact returns to two retirees.

Retiree A quits in January 2000 with $1,000,000 and pulls $55,000 a year, a 5.5% starting rate, never adjusting anything. He gets the returns in the order history actually delivered them. The dot com crash first, three red years in a row, then 2008 landing in year nine.

Retiree B gets the identical twenty returns in reverse order. The big years first, the crashes at the end. Same $1,000,000. Same $55,000 a year.

Retiree A runs out of money in year 20. Broke. Retiree B finishes with $1,703,688 and a crash he barely noticed.

Same average. Same twenty numbers. One goes broke and one grows his money by 70% while spending $55,000 a year, and the only difference is the order the returns showed up.

Chart summary. All three portfolios start at one million dollars in 2000 with $55,000 annual withdrawals. Bad order with no plan falls to $509,005 by 2002, partially recovers, drops to $315,795 after 2008, and hits zero in 2019. Bad order with the cut tiers and $15,000 of income in the first five years ends 2019 at $411,795. The reversed order with no plan ends 2019 at $1,703,688.

Two honesty notes on my own math. First, I didn’t even give these retirees inflation raises. Real spending grows over 20 years, and a properly inflation adjusted withdrawal would’ve sent Retiree A broke years earlier. My version flatters the no plan strategy and it still failed. Second, drop the rate to 4% and nobody goes broke, but the order still swings the outcome hard. A ends with about $865,000. B ends with $2.1 million. That’s a 2.5x gap from the exact same returns. Order barely touches the average. It decides everything at the edges, and a 40 year old retiree lives at the edges.

The first decade is the whole game

Michael Kitces has run the cleanest numbers I’ve seen on which returns actually matter. Across US history, the correlation between your safe withdrawal rate and your first year’s return is 0.21. Basically noise. The single worst first year any retiree ever faced, a 42% loss, still supported a 5.34% withdrawal rate over the full retirement. One crash doesn’t kill you.

A bad decade does. Widen the window to the first ten years of real returns and the correlation jumps to 0.79. Stretch it to fifteen years and it hits 0.91, while the correlation with full 30 year returns is a useless negative 0.09. Kitces said it plainly at a Schwab conference in late 2023, as reported by Financial Advisor magazine. Sequence risk “is mostly about what happens in the first decade after retirement.”

Morningstar’s December 2025 research found the same shape from the other direction. Portfolios that showed any gain over the first five years of retirement had roughly a 4% chance of ever running dry, and even one positive first year cut the failure risk in half. Survive the bottom of the mountain and the summit mostly takes care of itself.

Sequence risk punishes plans that were already leaking. My free guide covers the 10 quiet mistakes that kill early retirements before the market ever gets a swing at them. Grab it and check your plan against the list.

Send me the 10 mistakes

The 8% Crowd and the 3% Crowd Are Both Wrong

Sequence risk sits in a weird spot in the finance world. One camp pretends it doesn’t exist. The other camp uses it to scare you into products. Both cost you years of your life.

Start with the loud camp. In November 2023, a 30 year old called into The Ramsey Show asking about withdrawal rates for financial independence. Dave Ramsey told him 8% was fine. The logic went like this. Good mutual funds make 12%, inflation runs 4%, twelve minus four leaves eight, go spend it. Then he called the researchers behind the 4% rule “goobers and supernerds who have spent far too many hours in their moms’ basements.”

Dave, buddy. The market doesn’t pay 12% every year. It pays 28% one year, takes back 37% the next, and the average only works out on a spreadsheet where nobody has to eat. My twenty year series above averaged 7.68% and compounded at 6.06%, because volatility drags on real portfolios. Early Retirement Now ran the long version in its rebuttal that same month and put the real, inflation adjusted return of the S&P 500 from 1871 through late 2023 at 6.72% with dividends reinvested. Not 12. And in the years you lose 30%, drawing your full 8% guts the portfolio’s future permanently. That’s sequence risk eating you alive while the host laughs at nerds. For a 65 year old it’s irresponsible. For an early retiree it’s fatal.

Then there’s the quiet camp, and honestly they annoy me more. Nearly every big brokerage article on sequence risk ends the same way. A fat cash bucket, a bond ladder, maybe an annuity, definitely a call with their advisor. Morningstar’s latest report pegs the base case safe rate for a 40 year horizon at just 3.3%. And the fine print under numbers like that is always the same – they model a retiree who never adjusts spending by one dollar and never earns another dime for four or five decades.

I found that odd the first day I read this research and I find it odd now. You’re telling me a sharp 38 year old walks away from a career and then produces zero income for fifty years? That retiree doesn’t exist. The 4% rule carries the same assumption, which is a big part of why I already wrote that the 4% rule is too conservative. It’s a worst case output built from the worst case data, and your life is not the worst case dataset.

Don’t take my word on the conservatism. Take it from the man who invented the rule. Bill Bengen reran everything for his 2025 book A Richer Retirement and moved his own worst case number up to 4.7%. Across the 349 historical retirement dates he tested, the average rate that would have survived was about 7.1%. His famous floor exists because of one start date, October 1968, a retiree who walked into a decade of grinding inflation and two bear markets. Notice what that means. The worst case in a century of data wasn’t a crash. It was a bad decade, exactly what Kitces’ correlations predicted. And when Money magazine asked Bengen in August 2025 what he’d suggest for today’s retirees, the father of the 4% rule said “I’d probably recommend something around 5.25% to 5.5%.”

I run a 5.5% flexible plan. And the flexible part is what earns it, which is the rest of this article.

The Plan That Makes a Crash Survivable

Here’s my take, the one that gets pushback from both camps. Sequence of returns risk is the biggest single threat to an early retiree’s money, and it’s still not that big of a deal if you have a plan. The danger was never the crash. The danger is meeting the crash with no plan, because then you improvise, and people improvising with their life savings in the middle of a 35% drawdown make terrible decisions.

So decide everything now, while you’re calm.

My three cut tiers

If I retired tomorrow and the market fell 20% from its peak, I’d cut our spending 10 to 15%. At a 30% drop, 15 to 20%. At 40% or worse, as much as we could stand. I run an aggressive 5.5% starting rate, so I’ll be aggressive with the brakes too. Trimming the travel budget for eighteen months is a rounding error next to going back to work at 55.

| Market drop from its peak | My spending cut |

|---|---|

| 20% | 10 to 15% |

| 30% | 15 to 20% |

| 40% or more | As much as we can stand, 25 to 30% minimum |

Watch what those tiers do to Retiree A, our broke friend from 2000. I reran his twenty years with the cuts applied mechanically at the firm end of each range, 15, 20 and 30%, triggered by how far the market sat below its peak at the prior year’s close. The rules only fired in three years. Total spending over two decades fell by $30,250, which is 2.8%. And the ending balance went from zero to $110,498.

Read that again. The difference between broke and solvent was 2.8% of lifetime spending. Three lean years out of twenty.

Now, $110,000 after twenty years is alive, not comfortable. I won’t pretend the tiers alone turn the worst modern start date into a win. They’re one lever. Here’s the second, and it’s stronger.

The income lever nobody models

Add $15,000 a year of income for just the first five years. Same cuts, same everything else, and Retiree A finishes with $411,795. Income alone, with zero spending cuts, gets him to $275,614. Fifteen grand. Some consulting, a hobby that finally pays, a couple days a week doing something you’d honestly enjoy. About $75,000 of total earnings, positioned early, was worth roughly $300,000 of ending balance against the worst start sequence of the modern era, because every dollar you earn in a down year is a share you didn’t sell at the bottom.

| The 2000 retiree, 5.5% start | Balance after 20 years |

|---|---|

| No plan, fixed $55,000 every year | $0, broke in year 20 |

| Cut tiers only | $110,498 |

| Cut tiers plus $15,000 a year of income, first five years only | $411,795 |

| Same returns in reverse, no plan needed | $1,703,688 |

And this is where I lose people who think retiring early means taking a vow of unemployment. Retiring early means owning your time. Nobody handed you a rule that says you can’t earn a dollar with it. You’ve spent fifteen years building skills someone will pay for, and renting out a sliver of them on your own terms during your first few retirement years is the cheapest sequence insurance that exists. The brokerage articles never mention it because nobody earns a commission when you tend bar two shifts a week for a year.

The math on why those early dollars matter is brutal. Schwab’s research team ran a $1 million portfolio through two straight 15% loss years with $50,000 withdrawals coming out, then gave it steady 6% gains. At a 4% withdrawal rate during recovery, getting back to even takes 28 consecutive years. Cut withdrawals to 2% and it takes about 11.5. Withdrawals are the headwind. Shrink them when it matters and the portfolio heals itself.

The rest of my stack is shorter. A bucket holding one to two years of spending in cash and short bonds, built in the final stretch before the quit date, so a crash never forces a sale in year one. That’s the buffer I described when I wrote about staying 100% in stocks during accumulation, and it belongs to the guardrails family of strategies that researchers have refined since Guyton and Klinger’s 2006 work. Morningstar’s December 2025 report found flexible spending systems support starting rates as high as 5.7%, in the same research that caps the rigid version at 3.9%. Flexibility literally pays. And if the market looks stupid expensive the year I plan to leave, I’ll work six more months and let the picture clear. Whether I retire at 40 or 40 and a half changes nothing except my mood in meetings.

I’m not theorizing at you. I’m 33 with just under a million invested and a target of 40, and this exact playbook is what lets me plan around 5.5% flexible instead of hoarding 33 times my expenses like the 3% crowd wants. Write the plan once, and when the crash comes you just run the play. GGs.

Now the honest caveats, because I’d rather understate this than oversell it. Everything above is US market history, and the honest version of that promise is that the market has recovered every time so far. No guarantees live in this article, and if the next fifty years look like nothing in the last hundred, no withdrawal rate survives it, and neither does whatever an advisor sold you. My simulation also reads the market once a year at the close, which understates how often your tiers would actually trigger in real life, and skipping inflation flattered the no plan retiree most of all. If anything, reality rewards the plan more than my math does. And remember the floor. Bengen’s October 1968 retiree, the worst start in recorded history, still made it 30 years at a fixed 4.15% with zero flexibility and zero income. You’ll have two levers that retiree never used.

What to Do This Week

Don’t walk away from this scared of sequence risk. Walk away with a plan for it, because the plan is what lets you keep a higher withdrawal rate and an actual lifestyle instead of hiding behind 3% forever. If you only remember one sentence, make it this one:

Plan to adjust your spending based on the market.

This week, open a doc and write down four things. Your cut tiers, real percentages at real triggers, decided while you’re calm. The income you could plausibly generate in year one if the market fell apart, with at least one specific name or idea attached. The size of the cash buffer you’ll build in your final year of work. And if you’re married, book the conversation with your spouse. Who might keep working a little, what spending goes first, how much travel survives a bad year. My wife and I have had that talk. It took one evening and it’s worth more than any calculator output on this site.

The market will crash early in somebody’s retirement. Maybe yours. Maybe mine. The plan is the difference between a lean season and a ruined decade.

Before the market tests your plan, test it yourself. Get the free guide, 10 Quiet Mistakes That Kill Your Early Retirement, and find the leaks while they’re still cheap to fix.

Get the 10 mistakes

Sequence of Returns Risk FAQ

Does the 4% rule already account for sequence risk?

Yes. That’s the whole reason it’s so low. The 4% figure is the output of the single worst return sequence in US history, Bengen’s October 1968 retiree, who needed a rate near 4.15% to survive a brutal decade. If you’re willing to flex your spending or earn even a little income, you’re solving a problem that rule already assumed you couldn’t solve.

How long does sequence risk actually last?

The first decade carries almost all of it. Kitces found the first ten years of real returns correlate with your safe withdrawal rate at 0.79, and the first fifteen at 0.91, while the full 30 year return tells you almost nothing. Morningstar’s 2025 research adds that a portfolio with any gain over its first five years had only about a 4% chance of ever running out. Defend the front decade and you’ve defended the retirement.

Does sequence risk matter while I’m still accumulating?

No, and that’s a feature you should exploit. With no withdrawals there’s no forced selling, so a crash is a discount instead of a wound. I learned this the embarrassing way. I opened my brokerage in March 2020, put in $10,000 as COVID crashed the market, then sat frozen for two months while most of the rebound happened without me. In accumulation, freezing costs you gains. In withdrawal mode, the forced version of that mistake compounds against you forever, which is why the plan has to exist before the drop does.

Should I shift into bonds now to prepare for it?

Not during accumulation. I’ve made the case for staying fully in stocks while you build, and a 40 year old with a 50 year horizon still needs growth after quitting too. The move is a buffer, not a rebalance. One to two years of spending in cash and short bonds, built in the last year before you leave, then let the growth engine keep running behind it.

Simulation notes. Portfolio paths use S&P 500 total returns including dividends, 2000 through 2019, with withdrawals taken at the start of each year and no inflation adjustment. Cut tiers trigger on the index’s drawdown from its peak measured at the prior year end, at 15, 20 and 30% reductions. This is my own analysis and it’s for education, not personalized advice.